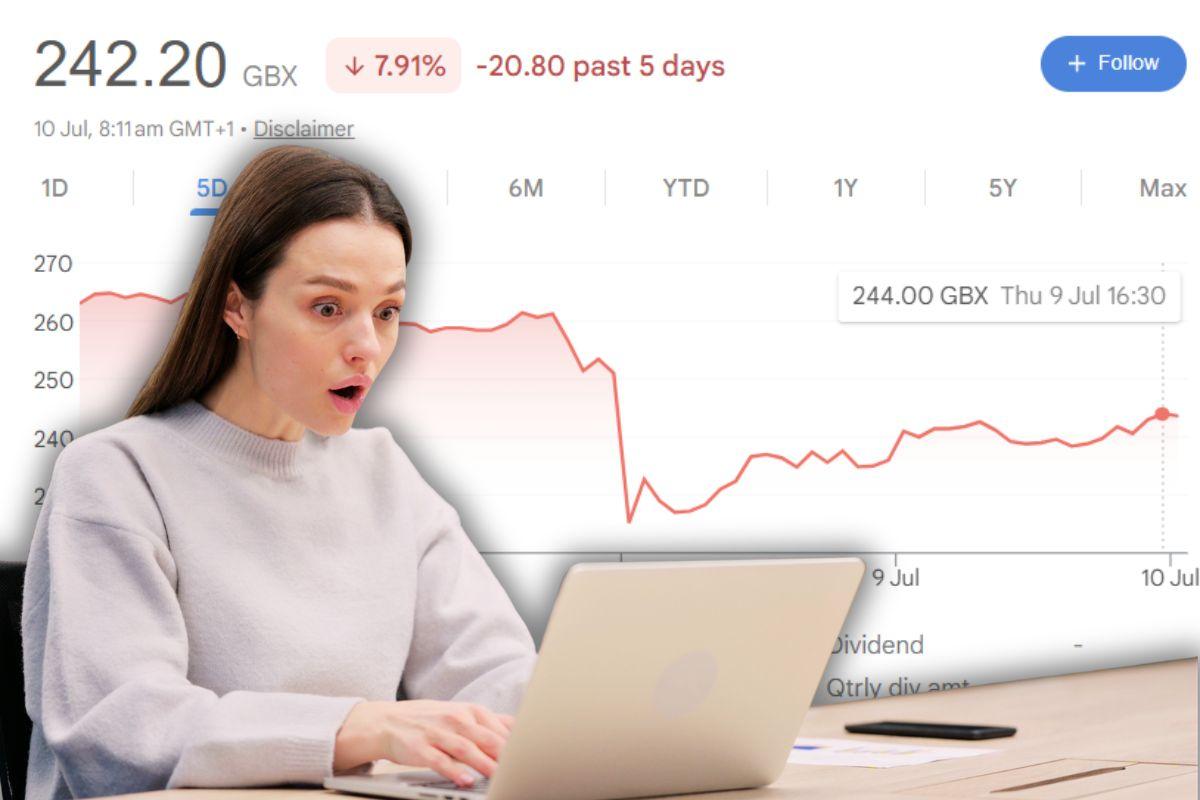

If you’d bought Vistry shares at the start of 2026, you’d have lost more than half your money by now. The stock hit 746p in February. It closed at 252.40p on July 7, then took another leg down on the morning of July 8, dropping more than 9% to around 229p after a fresh trading update. That’s not a correction. That’s a collapse, and it happened fast enough that a lot of shareholders are still processing it.

Vistry (LSE: VTY) is the UK’s largest housebuilder by volume. It builds under Bovis Homes, Linden Homes, and Countryside Homes, and runs a Partnerships division that works with housing associations, local authorities, and institutional investors to deliver affordable and mixed-tenure housing. A year ago, the investment case looked compelling. Now the shares are trading at levels that imply something close to distress, even though the business itself is not in that position. Understanding the gap between those two things is what this piece is about.

- Shares closed at 252.40p on July 7, then dropped another 9%+ on July 8 to around 229p after a shock trading update

- Vistry now expects a first-half pre-tax loss of around £30 million, not a profit, thanks to £50 million in discounting and inventory write-off costs

- CFO Tim Lawlor is out. He announced his resignation the same day as the loss warning and leaves by October

- The stock’s been as high as 746p and as low as 220p this past year, a near 60% fall from top to bottom

- That May 2026 profit warning ahead of the AGM knocked shares down over 10% in a single session, toward 264p

- Short sellers are circling harder than ever, with 12.5% of shares out on loan, a record for the company

- Full-year guidance got cut in May to £200-225 million, down from over £269 million, and Vistry stuck to roughly £200 million even after this week’s loss warning

- Adam Daniels became CEO back in April. His big operational review lands September 24, the same day as half-year results

- No dividend, and the buyback’s been paused

October 2024: Where It Actually Started

To understand the Vistry share price today you have to go back to October 2024. The company announced it had discovered that cost projections across nine developments in its South Division had been understated by around 10% of total build costs. Not across the whole business, nine sites out of roughly 300, but the market didn’t read it that way. More than £1 billion came off the market cap in a single session. The stock was one of the worst performers on the FTSE 100 that day.

What made it worse was the timing. Vistry had been actively positioning itself as the smart play in UK housebuilding, pivoting away from the traditional build-and-sell model toward its capital-light Partnerships approach. Investor sentiment had been building. The announcement shattered that narrative overnight, and the trust it took months to build came undone in hours.

Also Read: Is NIO a Good Stock to Buy? Learn About EV Market Potential

2026: Trying to Stabilise and Failing

The company spent the first months of 2026 trying to convince the market things were under control. Full-year 2025 results in March showed net income of £138 million, earnings per share recovering to £0.42 from £0.22 the year before, and a share buyback programme that had spent around £130 million in 2025 buying back stock at prices between 337p and 343p. In hindsight, that looks like burning money, given where the shares are now.

On the day those results came out, the stock fell another 20%. Not because the numbers were bad exactly, but because the guidance for the first half of 2026 was. Excess inventory on completed and near-completed homes, particularly in the South East, was being cleared through heavy discounting. Sales volumes were up 32% year on year. Margins were not.

Then came May 13. Ahead of the AGM, Vistry issued another trading update. First-half profits for the six months to June 30 would be significantly lower than the same period in 2025. The discounting was hitting harder than the market had modelled. Shares fell 10.6% to 288.8p on the day. Jefferies cut its 2026 profit forecast from around £250 million to somewhere between £200 and £225 million. Peel Hunt trimmed by £15 million to £210 million. Stifel, which had put a Buy rating on the stock in March, said the upgrade had been made too early. The buyback was suspended. Full-year profit guidance was maintained but at the middle of the analyst range of £168 million to £283 million, which is a pretty wide range and tells you how uncertain the picture genuinely is.

Within a fortnight the shares had drifted from 331p to 264p. Short interest jumped to 12.5% of shares out on loan, the highest it had ever been for Vistry. Housing Today quoted a source at the company saying short sellers were “contributing nothing” to UK housing needs. The shorts didn’t much care.

The slide didn’t actually stop there. Through June, the shares kept grinding lower, drifting down toward the 220p 52-week low before steadying a bit in the 240p to 252p range going into July. Then July 8 hit. Vistry put out another trading update, this time saying it now expects a first-half pre-tax loss of around £30 million, a swing from what would’ve been roughly £20 million in profit without around £50 million in one-off costs from accelerated discounting, asset sales, and write-downs on low-margin sites. CFO Tim Lawlor announced his resignation in the same update, agreeing to stay through October while the company finds a replacement. Shares fell more than 9% in early trading to around 229p. The one bit of good news buried in there: Vistry held its full-year guidance at around £200 million, in line with what analysts were already expecting.

Also Read: Highest-Paying Sectors in the UK With Strong Career Growth

What the Business Looks Like Right Now?

At 252.40p, last night’s close before today’s fall to around 229p, Vistry was trading at roughly 0.28 times tangible book value. A PE ratio of 6.21. A forward order book of £4.5 billion. Year-end net cash guided at more than £100 million. These are not the numbers of a company heading toward administration. They’re the numbers of a company that has had a rough eighteen months and is being priced as if the rough patch is permanent.

The Partnerships division is the piece that long-term investors keep pointing to. It builds homes where the buyer, whether that’s a housing association, a local authority, or an institutional fund, has committed to purchasing them before construction begins. That removes the inventory risk that has hurt Vistry’s open market operations so badly when private buyers pulled back. The company is one of the best-placed operators to benefit from the government’s £39 billion Social and Affordable Homes Programme running from 2026 to 2036. That funding creates structural demand that doesn’t disappear when mortgage rates tick up.

The problem is that between now and the point where that structural demand fully kicks in, there’s still a difficult period to get through. Peel Hunt noted that the transition between government affordable housing funding programmes had temporarily suppressed Partnerships activity. Grant announcements expected in Q3 2026 should help that, but “should help” is doing a lot of work in that sentence for anyone who’s watched the guidance repeatedly disappoint.

New CEO, Operational Review, and the September Date

Adam Daniels took over as CEO on April 13, 2026. He’s not an outsider parachuted in to restructure. He joined Countryside Partnerships in 2016, spent a decade inside the business, and has relationships with many of the housing associations and local authorities that are Vistry’s core Partnerships customers. The board also changed at the AGM, with Rob Woodward CBE replacing Greg Fitzgerald as Non-Executive Chair after Fitzgerald stepped down.

The AGM itself was uncomfortable. Around 37% of shareholder votes went against both the remuneration report and remuneration policy. That level of dissent, from institutional investors who usually vote quietly in favour of whatever management proposes, signals something beyond routine discontent.

Daniels’ operational review is due September 24, 2026, the same day as the half-year results. That double announcement is the single most important date in Vistry’s calendar for the rest of this year. It’s when investors will find out whether the H2 recovery management has been guiding for is actually showing up in the numbers, and what strategic changes Daniels thinks are necessary to fix what’s broken.

The analyst consensus is a Hold with a price target of 356p on Stockopedia’s aggregated data, implying meaningful upside from the current price. But Hold ratings and price targets have been cut repeatedly over the past year, and at this point the stock needs delivery rather than guidance to move the dial.

Also Read: 15 Legitimate Work From Home Jobs With Flexible Hours

FAQs

What is the Vistry share price right now?

Vistry closed at 252.40p on July 7, then dropped over 9% in early trading on July 8 to around 229p after a fresh warning, putting the business at roughly £725 million. The 52-week range is 220p to 746p, and the stock’s down more than 58% over the past year. Worth checking a live price feed since it’s still moving.

Why has the Vistry share price fallen so much?

It goes back to October 2024, when the company admitted it had understated build costs on nine South Division developments, wiping over £1 billion off its value in a day. Then heavy discounting to clear excess stock crushed margins through 2026 and led to repeated profit warnings. Short sellers piled on top of that, with a record 12.5% of shares out on loan. And this week’s news, a swing to a first-half loss plus the CFO walking out the door, dragged it down again toward the 52-week low.

Is Vistry paying a dividend?

No. There’s no dividend right now, and the buyback that spent around £130 million in 2025 is paused too. The company’s putting cash toward debt reduction instead of shareholder returns for the time being.

What do analysts actually think about VTY?

Consensus is Hold. Price targets differ across platforms, but they all sit above where the stock’s trading now. The catch is analyst forecasts for full-year profit span £168 million to £283 million, which is a huge range and shows just how much uncertainty is still baked in.

When is the next major Vistry announcement?

September 24, 2026. That’s when the full half-year results land alongside Adam Daniels’ operational review. Vistry already gave a rough preview of the H1 numbers in the July 8 trading update, warning of a swing to a loss, but the full picture and any further hits from the review are still to come. Government grant announcements for affordable housing, expected in Q3 2026, are also worth watching as a potential trigger for the Partnerships side of the business.

Is Vistry actually the UK’s biggest housebuilder?

By volume, yes. It runs under Bovis Homes, Linden Homes, and Countryside Homes, plus the Partnerships division. Founded in 1885 as Bovis Homes, renamed Vistry Group in January 2020 after the Countryside Partnerships acquisition.

Sources and References

Vistry Share Price Today, ADVFN

Vistry Share Price Forecast and Financials, Stockopedia

Vistry Shares Under Pressure as Brokers Cut Profit Forecasts, Yahoo Finance

Vistry Shares Slide Again as Profit Warning and Debt Concerns Deepen, AskTraders

Vistry Share Price Tumbles Amid Rise in Short-Selling Activity, Housing Today

Vistry Group Stock Analysis, Simply Wall St

Vistry Shares Down 20%, The Motley Fool UK